{kind=link}

This Article pertaining to “GSTAT Deadline: Extending Time, Strengthening Trust” is written by Dr Monish Bhalla. He is a distinguished author, legal expert, and former officer of India’s Narcotics Control Bureau (NCB). With 37 years in public life, Dr. Bhalla has been a key figure in drug law enforcement and indirect taxation in India. His expertise in the fields of GST, Customs, and narcotics control has made him a leading voice in legal reforms and national policy. He is also a well-known columnist and has authored several books on GST, drug trafficking, and legal matters.

It is time for a balanced approach that protects revenue while keeping justice within reach of taxpayers.

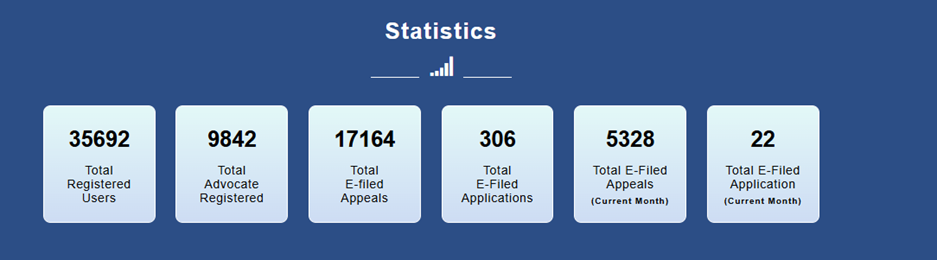

Eight years after GST was introduced, India’s tax litigants are facing a serious problem. The newly operational GST Appellate Tribunal, GSTAT, has fixed 30th June 2026 as the final deadline for filing backlog appeals. However, against an expected four to five lakh appeals, only 17,164 appeals have been filed so far.

In other words, only about 3 percent of the expected appeals have been filed till date, while nearly 97 percent are still to be filed in less than two weeks. This is not a small procedural lapse. It is a clear sign that something is seriously wrong.

This huge gap does not show that taxpayers are careless or unwilling to file appeals. It shows that there are practical and systemic barriers which have made the appellate process difficult, and in many cases almost unreachable, for ordinary businesses.

Source: GSTAT PORTAL

The real question, therefore, is not whether the deadline should be extended merely for administrative convenience. The real question is whether fairness and justice require such an extension when the system itself has not provided taxpayers a proper and meaningful opportunity to file their appeals.

What, then, is stopping taxpayers from filing appeals in time?

Many experts believe that the biggest obstacle is the mandatory pre-deposit requirement. This has become one of the most serious barriers to justice under the GST regime. Before filing an appeal before the GST Appellate Tribunal, a taxpayer is required to deposit 100 percent of the admitted tax and an additional 10 percent of the disputed tax. This comes on top of the 10 percent already deposited at the first appellate stage.

This requirement has created a rigid system. In practical terms, the right to appeal now depends on whether the taxpayer can arrange the required amount upfront. For many businesses, especially small and medium enterprises working on thin margins, this is not easy.

The pre-deposit amount blocks valuable working capital. This is money which could otherwise be used to run the business, pay salaries, clear dues, purchase raw material, or keep operations alive. As a result, many taxpayers may be forced to give up even valid appeals, not because their case is weak, but because they cannot afford to keep such a large amount locked up.

For such businesses, the appeal process becomes less about justice and more about financial capacity. That is where the real concern lies.

The bitter truth is that the financial hardship caused by the pre-deposit requirement is not just a matter of theory. It is a real and practical barrier which has slowed down, and in many cases almost paralysed, the appellate process.

This becomes even more serious because GST appeals may take years to reach final disposal. The backlog has been building up since 2017, covering almost eight years of GST implementation. This means that even after filing an appeal, taxpayers may have to wait for a long time before their cases are finally decided.

Litigation under the GST regime has already placed a significant burden on appellate forums, including the proposed GST Appellate Tribunal. Neutral reviews of tax litigation indicate that at the tribunal and higher court level, the tax department succeeds in roughly 20 to 30 out of every 100 cases, with the remaining matters decided wholly or partly against it.

The tribunal is still in its early stage of functioning, and hearings have yet to begin in a regular manner. In such a situation, businesses face a very difficult choice. They must either accept a demand which they may genuinely believe is wrong, or they must file an appeal and keep their money locked in pre-deposit for years. For many businesses, this is not just a legal decision. It is a question of financial survival.

Apart from the burden of pre-deposit, the GSTAT e-filing portal has also created serious difficulties for taxpayers. Many taxpayers have faced repeated technical glitches while trying to file appeals. Authentication delays, problems in synchronization between the GST portal and the GSTAT platform, and OTP-related issues have stopped or delayed filings, even where taxpayers were ready to comply.

When these technical problems are seen together with the heavy pre-deposit requirement, the result is a very difficult system for taxpayers. The financial burden makes appeals costly, and the portal-related difficulties make filing slow and frustrating. For many ordinary taxpayers, filing even a single appeal has become an exhausting task.

Despite all these concerns, the case for extending the deadline remains strong when seen from the angle of fairness, justice, and constitutional principles.

The right to appeal is not an empty procedural formality. It is an important legal right. If the conditions attached to filing an appeal make it impossible for a large number of taxpayers to exercise that right, then the system fails in its basic purpose.

Our Constitution guarantees equality before law. But if the appellate process is practically available only to those who have enough financial strength, then this principle gets weakened. Justice cannot depend only on the taxpayer’s ability to arrange money for pre-deposit.

Justice cannot depend only on the taxpayer’s ability to arrange money for pre-deposit.

The present filing position itself shows the problem. If only around 3 percent of the expected appeals have been filed so far, it is clear that the system is not working as it should. The government has also indicated that it may consider extending the deadline, if required. Such an extension should not be seen as a concession to taxpayers. It should be seen as a practical correction to ensure meaningful access to justice.

If the deadline is not extended, taxpayers will have very limited options. Most of these options carry serious risks.

One possible remedy is to approach the High Court by filing a writ petition under Article 226 of the Constitution. However, success in such petitions is not easy. Courts do not normally interfere where the delay is seen as ordinary negligence, portal difficulty, financial hardship, or lack of awareness of the deadline.

The practical reality is harsh. If the 30th June deadline is missed, the taxpayer may permanently lose the right to appeal. Once that happens, the demand becomes final, and the taxpayer may be left with no effective remedy.

That is why the issue is not merely about extending a date. It is about protecting the right to appeal and ensuring that justice remains available not only in law, but also in practice.

That is why the issue is not merely about extending a date. It is about protecting the right to appeal.

It is time to think out of the box. Routine remedies may not be enough. The government should consider a practical solution which goes beyond a simple extension of the deadline.

One possible way forward could be a special amnesty-type scheme. Under such a scheme, taxpayers who have missed the appeal deadline may be allowed to file their appeals, subject to payment of pre-deposit. However, instead of asking them to pay the entire amount at once, the government may permit them to pay it in installments up to a fixed date, say 31st December 2026.

This would give genuine taxpayers some breathing space. At the same time, the government’s revenue interest would also remain protected.

The government may also consider linking this relief with the relaxed scrutiny framework, which has already been extended up to 31st December 2026. This framework can be expanded to cover cases where appeals were filed before 30th June, but defects are still required to be cured.

The GST Council and the Ministry of Finance may also consider special relief for small businesses. In such cases, the pre-deposit requirement may either be reduced or allowed to be paid in phases.

Many small taxpayers may have genuine cases on merits, but they may not be in a position to arrange a large pre-deposit immediately. For them, the issue is not unwillingness to comply. The issue is financial capacity.

A balanced approach will give real relief to taxpayers without weakening the legal framework. It will also show that the government is willing to listen, understand practical difficulties, and still maintain the discipline of law.

The way forward is to accept one basic fact: when strict legal requirements make access to justice difficult or almost impossible, they need to be reviewed and adjusted. The purpose of law is not only to enforce deadlines, but also to ensure that justice remains available in a real and meaningful way.

The success of GST does not depend only on tax collection. It also depends on the confidence of taxpayers that their disputes will be heard fairly. If taxpayers feel that they cannot challenge a wrong demand because of heavy pre-deposit, technical problems, or procedural hurdles, their faith in the system is bound to suffer.

Extending the GSTAT deadline is no longer just a matter of convenience. It is a matter of fairness. But the extension must not stand alone. It should be supported by practical steps such as easing the burden of pre-deposit, allowing flexibility in genuine cases, and making the GSTAT portal simpler and more reliable.

GST was built on the promise of a fair and transparent tax system. That promise can be fulfilled only when taxpayers are given a real opportunity to challenge demands which they believe are wrong. No taxpayer should be forced to give up a valid appeal merely because of financial pressure, technical hurdles, or procedural complications.

No taxpayer should be forced to give up a valid appeal merely because of financial pressure, technical hurdles, or procedural complications.

A fair extension, backed by practical reforms, would strengthen both justice and the credibility of GST. It would send the right message: the system is not only interested in collecting revenue, but also in ensuring that justice remains within reach of every taxpayer.

Read More: Road Construction Services Exempt and SCN Time-Barred: CESTAT Quashes Service Tax Demand Based Solely on Form 26ASGST Full Form And Meaning : EXPLAINED