NATIONAL ACADEMY OF CUSTOMS INDIRECT TAXES AND NARCOTICS")

{kind=link}

The Article “From Seizing/freezing to forfeiture: Unmasking Section 68J of NDPS Act” is written by SRINIVASAN GOPAL, ASSISTANT DIRECTOR(RETD.) NATIONAL ACADEMY OF CUSTOMS INDIRECT TAXES AND NARCOTICS. Srinivasan Gopal is a distinguished retired Assistant Director of the National Academy of Customs, Indirect Taxes and Narcotics (IRS), recognized for his doctrinal scholarship and global outreach in narcotics law enforcement.

Introduction

It is generally assumed that arrest provisions lie only in Chapter V of the NDPS Act (in short, ‘the Act’). However, a careful reading reveals that Chapter VA also vests arrest powers in empowered officers.

Chapter VA proceedings deal with illegal acquiring of property. A person may not ‘touch’ drugs and he may be the kingpin/mastermind operating from behind the scene. He may appear legitimate—operating businesses or philanthropic ventures—while laundering proceeds of crime. Essentially, these seemingly legitimate ventures—realtors, philanthropists, or businessmen—perfect the art of masking illicit proceeds of drug trafficking, a technique that demands equal expertise in unmasking and exposing the concealment.

Chapter VA was inserted into the Act vide Section 19 of Act 2 of 1989 and came into force from 29 May 1989 and the Chapter VA was titled as “Forfeiture of property derived from, or used, in illicit traffic”. However, the title was substituted vide Section 19 of Act 16 of 2014 and came into effect from 01 May 2014.

The change of title was essentially clarificatory, not substantive. To understand this, we refer to the I988 International Convention for a proper understanding of the Article 5 vis a vis Chapter VA of the Act.

| Article 5 of 1988 International Convention | Chapter VA of the Act | Remarks |

| Confiscation of proceeds (Art. 5(1)) | Sections 68C–68I: forfeiture, Competent Authority, Tribunal | Civil forfeiture provisions under Sections 68C–68I directly mirror Article 5(1), adopting a property‑focused model. |

| Identification, tracing, freezing (Art. 5(2)) | Attachment, notice, adjudication Section 68F read with Section 68J | Quasijudicial model chosen |

| Criminalisation of possession, concealment, transfer (Art. 5(3)) | Direct mirror of Convention | |

| Judicial/administrative procedures | Appeals to Appellate Tribunal | Administrativejudicial hybrid |

| Evidentiary hurdles | Burden of proof shifted to accused | Operational safeguard |

| Competent Authorities must have adequate powers | Competent Authority & Tribunal vested with powers of a Civil Court | Mirroring the provisions of the Convention |

The International Mandate under Article 5 of the 1988 Convention and its correlation to Act

As can be seen from the Table Article 5 obligates States to confiscate the proceeds of drug offences ((Art. 5(1)), Identify, trace, freeze, seize such proceeds (Art. 5(2)); Acts of conversion, transfer, concealment, disguise, or possession of illicit proceeds, knowing they are derived from drug offences (Art. 5(3)).; Provide judicial or administrative procedures for confiscation and Cooperate internationally in tracing and confiscating assets.

In India, we have in place mirroring the provisions of the 1988 Convention. The empowered officer under Section 53 is to cause financial investigation under Section 57A. While this is a standalone provision, it has to be read in conjunction with the provisions of Chapter VA, which mandates the empowered officer to identify the illegally acquired property and take all steps necessary for tracing and identifying such property under Section 68E. He must then issue a Seizing or Freezing Order and the Competent Authority, appointed under Section 68D, is required to confirm the order within a period of 30 days of the issuance of same. The empowered officer is required to transmit the seizing or freezing order within 48 hours of its being made.

While the Convention mandates confiscation of the properties in question, we have made a stark difference in as much we have adopted a hybrid model and we have a concept of forfeiture introduced.

Chapter VA proceedings

Illicit property—being the proceeds of illicit drug trafficking—takes the forfeiture route under Chapter VA, a civil action before the Competent Authority and Appellate Tribunal. Conveyances purchased out of such proceeds, even where no recovery has taken place from them, also fall within the ambit of Chapter VA proceedings. By contrast, drugs, articles, and conveyances used in trafficking are subject to confiscation under Chapter V by the Ld. Trial Court. Importantly, Section 60(3) carves out an exception: pilot or escort vehicles from which no drugs are recovered remain outside the court’s confiscatory powers. This statutory design underscores the deliberate distinction between civil forfeiture of illicit assets and judicial confiscation of trafficking instruments—a distinction that is doctrinally critical and must never be blurred.

The administrative powers equivalent to the judicial process of confiscation has been termed as ‘forfeiture’. The person affected by the decision has been given the right to take the matter to the Appellate Tribunal, constituted under Section 68N, twice – first when the freezing or seizing order is confirmed by the Competent Authority and for the second time, when the Competent Authority forfeits the property.

Sections 68C to 68I establish the civil machinery: attachment, notice, adjudication, forfeiture, and appeal. These are quasijudicial proceedings, focused on property. They mirror Article 5(1) & 5(2). India chose a quasijudicial model, with Competent Authority and Appellate Tribunal, rather than purely judicial confiscation.

Burden of proof

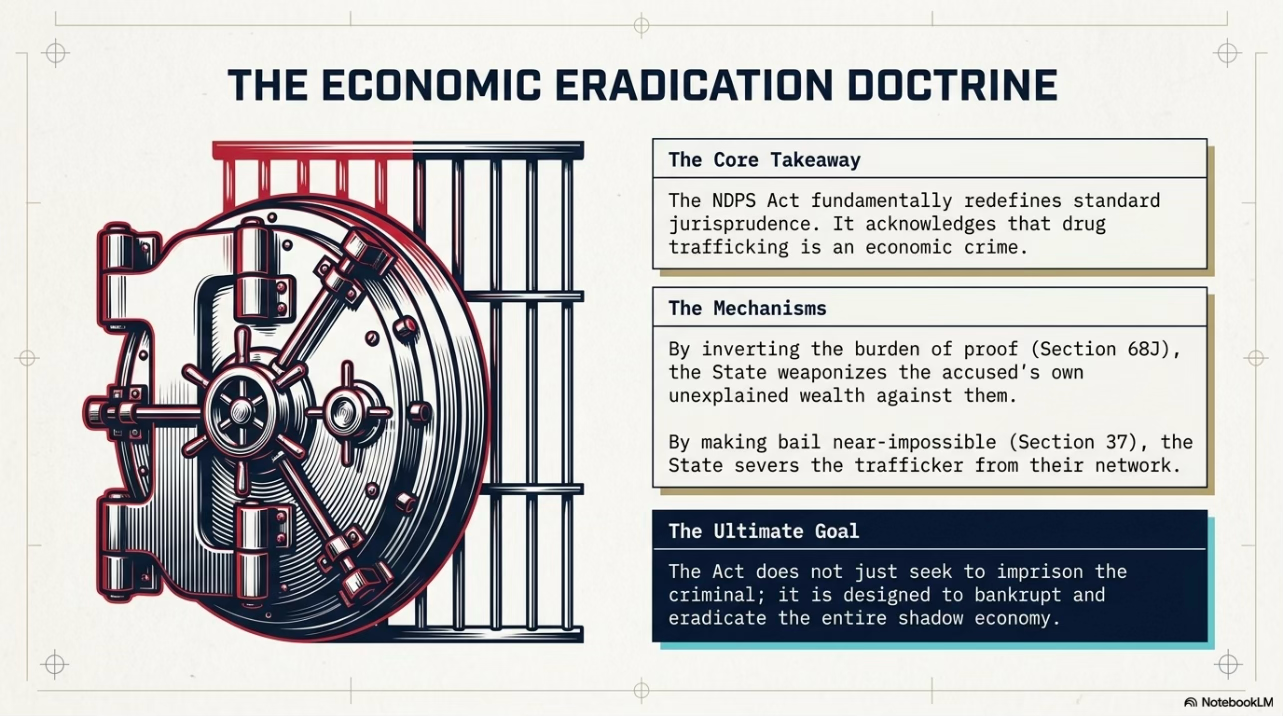

Section 68J, rightly so, shifts the burden of proof to the person from whom the property was seized or frozen. It is for him to disprove the theory floated by the empowered officer/department. Essentially, it is a case of reverse burden. This is akin to Section 123 of the Customs Act, 1962 where the burden to prove that he has not indulged in smuggling of the notified goods (viz. gold/silver and manufactures thereof, cigarette, firecrackers, etc)

Illustration

Chapter VA proceedings are attracted only in commercial quantity cases, where punishment is ten years or more, or in respect of PITNDPS detenus who have completed the full period of detention without revocation of the order by the High Court or Supreme Court. Intermediate quantity cases remain outside its explicit ambit. This statutory gap has emboldened traffickers to deliberately deal in intermediate quantities, exploiting bail provisions and evading forfeiture, effectively playing with the law while continuing to accumulate illicit assets.

Covering the intermediate quantity of drugs under Chapter VA (since it is upto 10 years and the Ld. Trial Court can award 10 years too) found judicial echo in Safik Laskar @ Safiqul Laskar @ Pintu & Ors. vs. The State of West Bengal & Ors. – Neutral Citation 2025:CHC-AS:1868.

Effective use of Section 68J

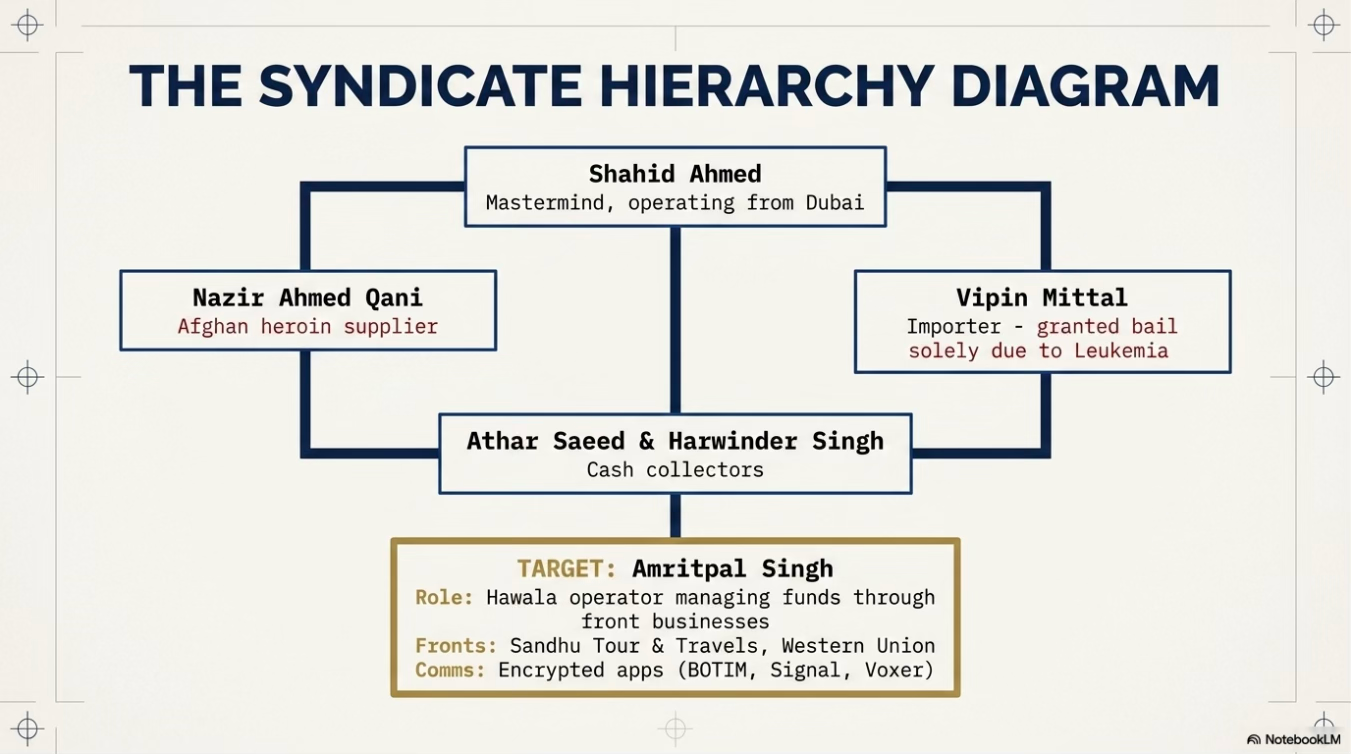

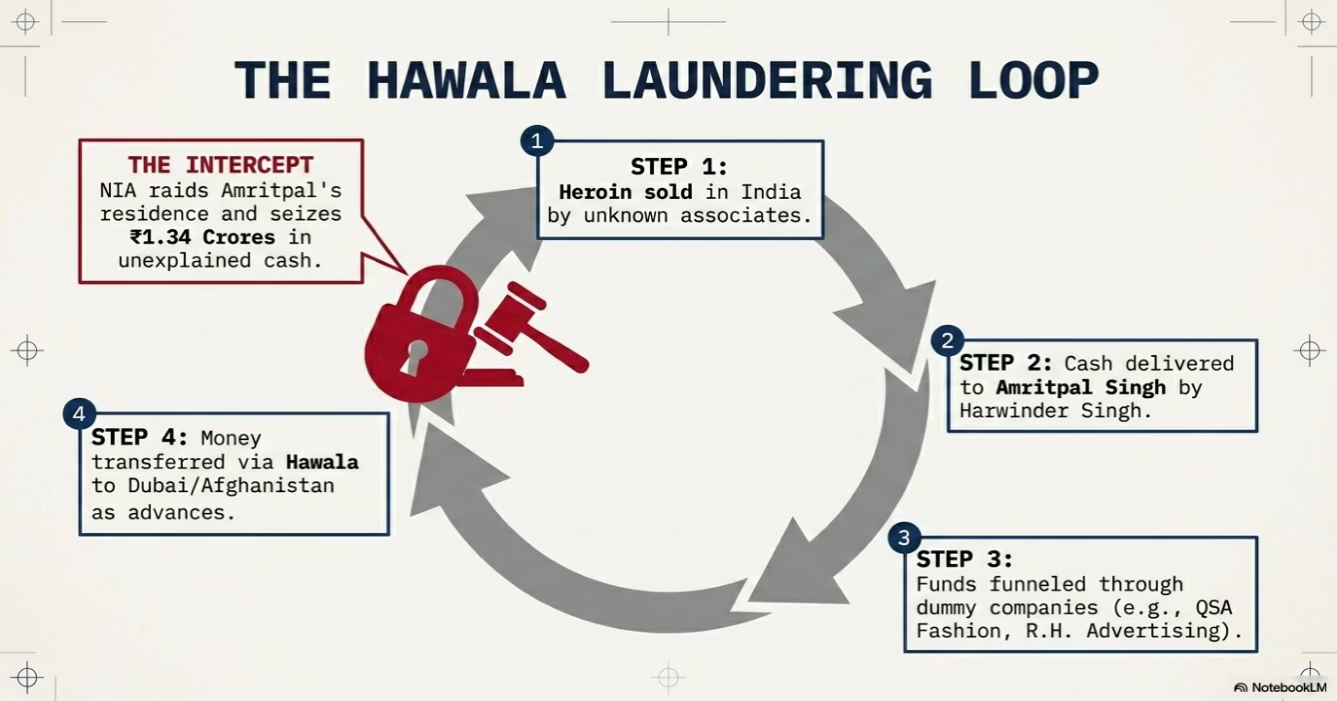

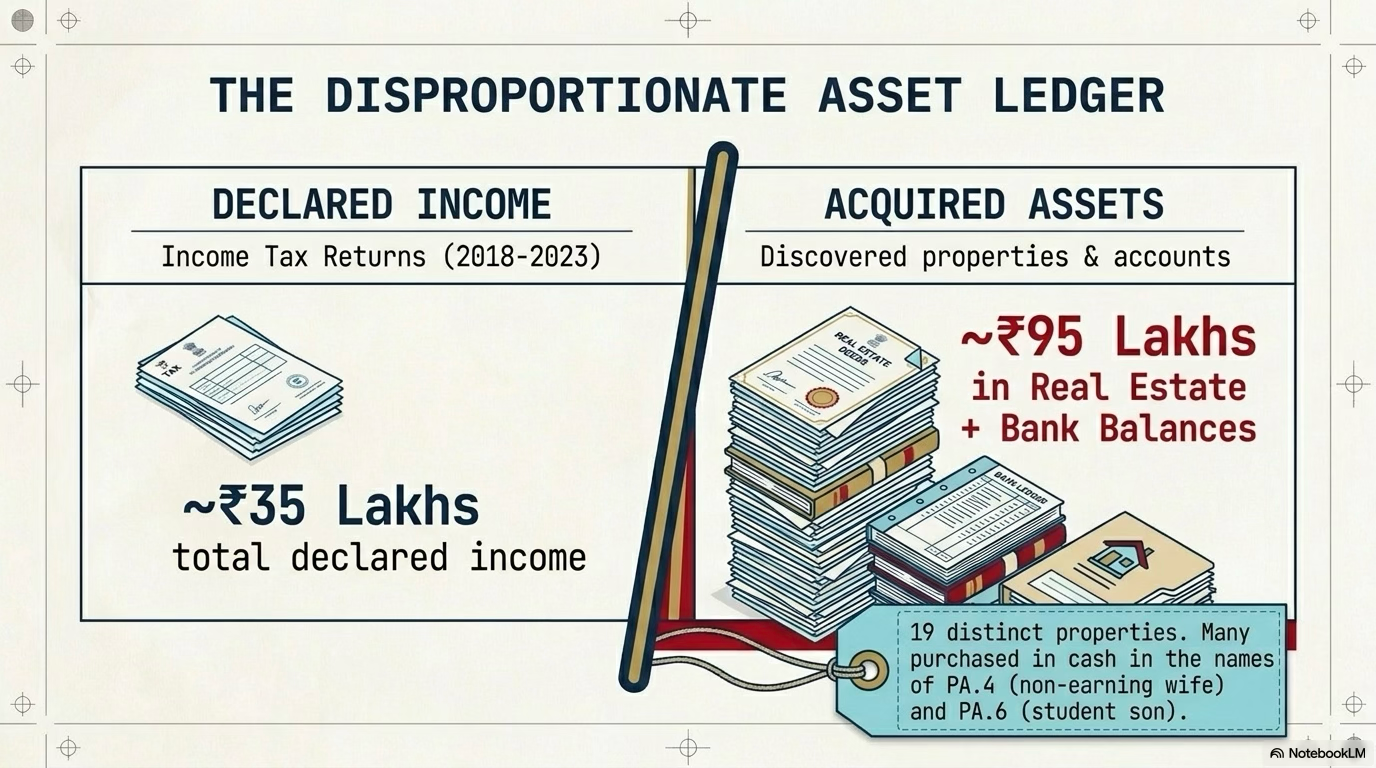

Jails often function as incubators of crime where meetings of minds take place and future illegal business deals are forged. The handler or mastermind remains in safe places, insulated from direct exposure, while identifying persons to act as conduits for transfer of money. Initially, legitimate businesses are used to camouflage the flow of funds, and later front companies or shell entities are floated to provide visibility and a façade of legitimacy. Those involved in such operations indulge in drug trafficking without any moral restraint, driven by the lure of quick money at the cost of the public. The assets they accumulate—whether movable or immovable, cash in hand or deposits, corporeal or incorporeal—are disproportionate to their legitimate earnings and consequently attract Chapter VA proceedings by way of freezing or seizing. In their eagerness to rise quickly in the criminal ladder, individuals get entrapped in these networks. It is in this context that financial investigation assumes paramount importance, for it unmasks the concealed proceeds of drug trafficking.

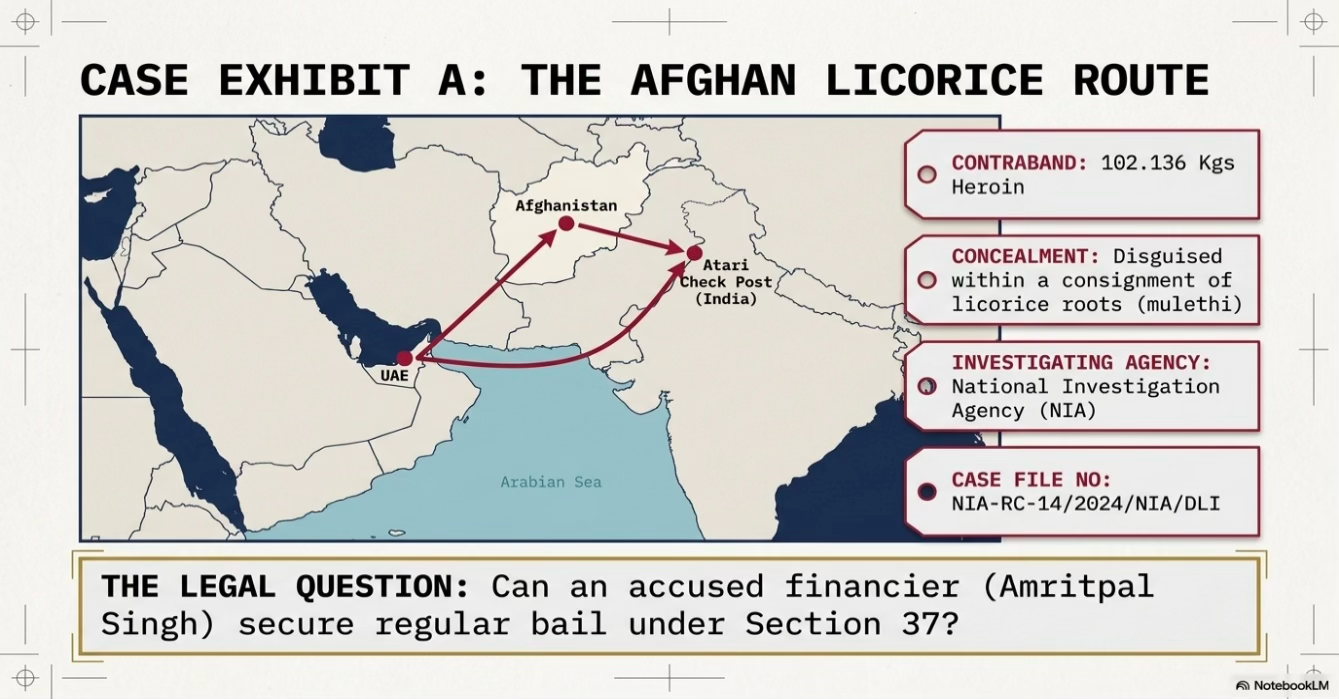

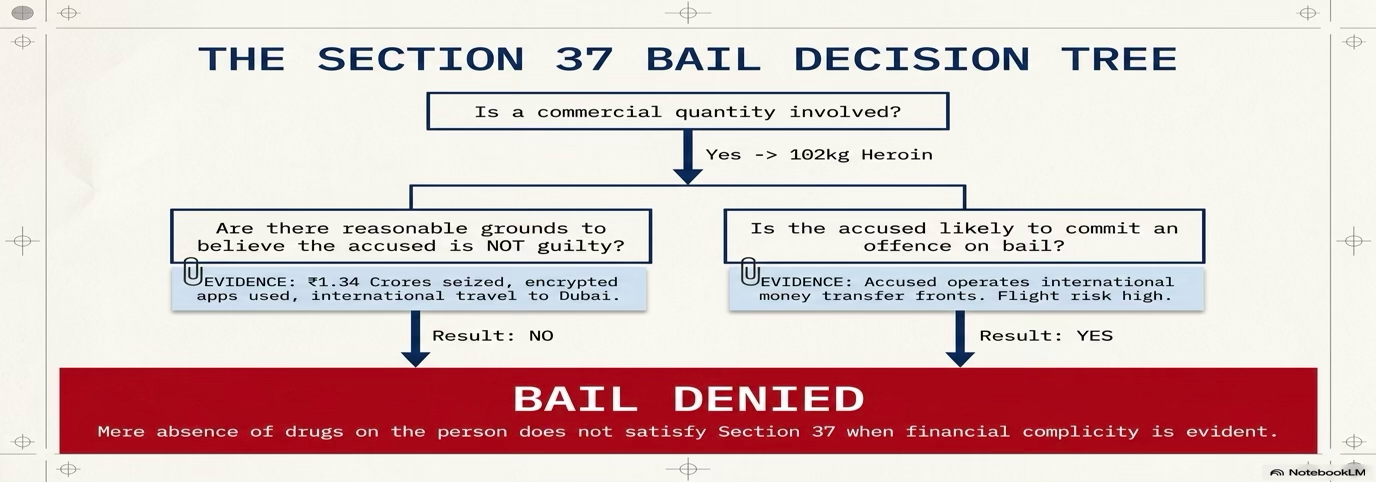

The recent decisions illustrated in Amritpal Singh vs. National Investigation Agency (2024:DHC:9365), which brings out the essence of the case wherein normal citizens got entrapped in the cyclic game of illicit drug trafficking, without knowing the effect of their consequences.

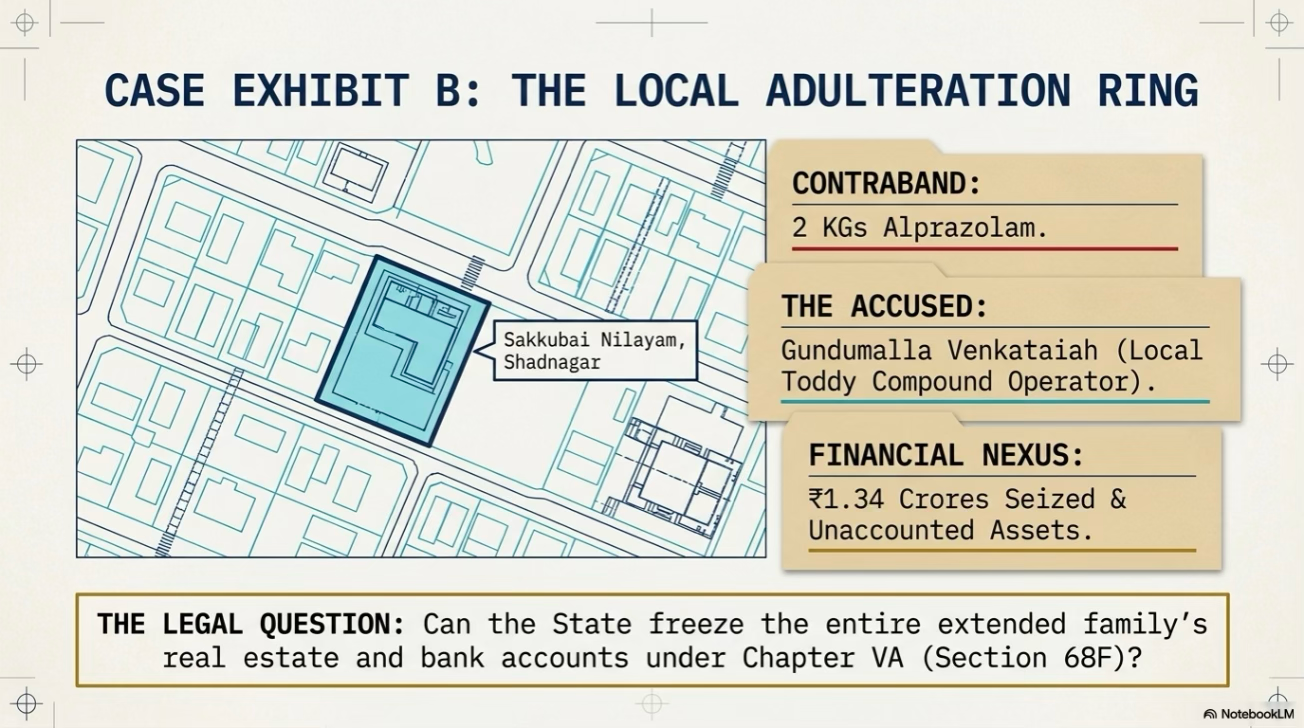

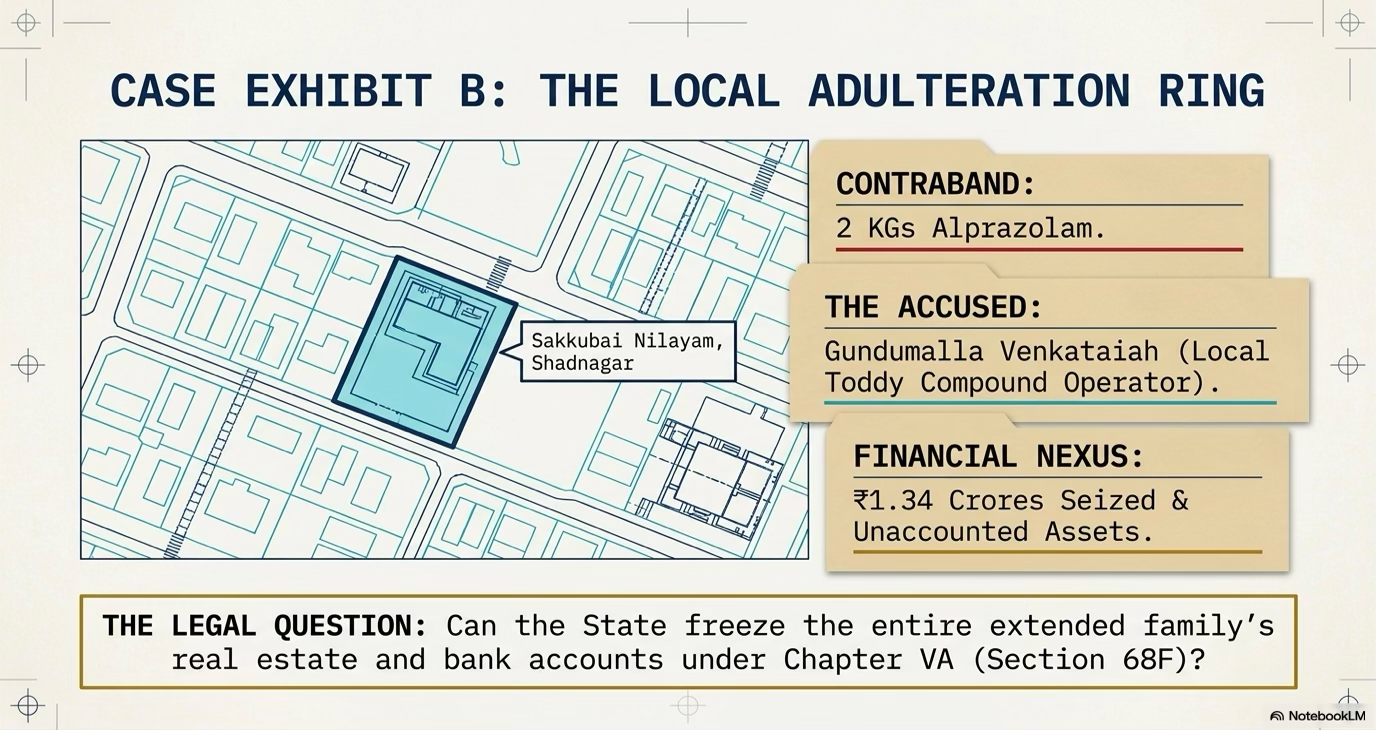

Similarly, in the second illustration, persons operating well within the country can be witnessed inGundumalla Venkataiah vs. Union of India -LAWS(TLNG)-2025-4-8 and this case brings out the Chapter VA proceedings effectively. The freezing of immovable and movable properties in these two cases under two different extreme circumstance only goes on to prove and establish that Section 68J is the powerful arsenal in the armoury of the prosecution but only comes to their rescue when financial investigation is conducted.

Alprazolam is the psychotropic substance which is laced with toddy to give the additional ‘high’ to the consumers and that is one of the reasons we find many clandestine bust of factory/lab busts in the Andhra Pradesh/Telangana States. If not done here, it is done in other States and importer inter-State into Andhra Pradesh and Telangana. The case involving Gundumalla Venkataiah is no different in the illicit drug trafficking and accumulation of assets.

The mighty Section 68J

Section 68J, is the most powerful tool to unlock the potential proceeds of illicit drug trafficking in whatever form they exist—tangible or intangible, movable, or immovable, corporeal or incorporeal. There can be no better provision in the entire Act than Section 68J to neutralize the proceeds of illicit drug trafficking and bring them within the reach of enforcement.

Conclusion

These two classic examples illustrate that a properly conducted financial investigation can unearth movable and immovable properties of all kinds, whether held in one’s own name or in the names of relatives or associates, and cause disruption by bringing about an economic meltdown of illegally acquired assets.